EFT-1 was a one-off demo launched in 2014 with a boilerplate Orion Capsule. SLS and Orion have been continously delayed despite multiple billions of dollars per year of funding. SpaceX launched Falcon Heavy earlier this year and plans to launch this configuration 1-2 more times this year.

I recently read an article from Spacenews titled 'Boeing, Lockheed, ULA corner the government-funded space market. SpaceX moving up' by Sandra Erwin and some points stood out to me. Specifically, while the article is well-written and researched, in my opinion it approaches the discussion from the completely wrong point of view. New Space companies like SpaceX and Blue Origin are disrupting the global launch market, not only the U.S. government launch market. Also while the impact of these companies have been dramatic, they focus on narrow niches while the vast majority of government space contracts do not have real private sector competitions.

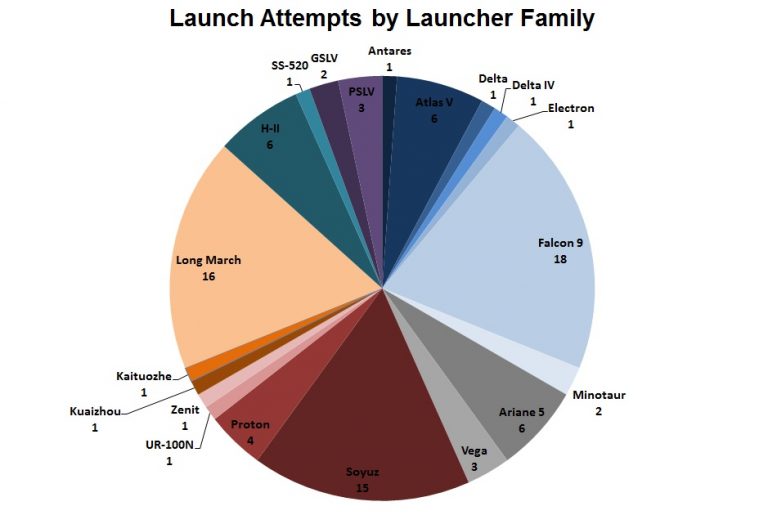

The Collapse and Rebirth of U.S Launch

2017 was an inflection point, where the US launched more rockets for the first time since 2003. Via spaceflight101.com

Yes, considering only U.S. dollars spent on space-related technologies, traditional government contracts have a huge institutional advantage. However, when the author says ULA has 49% of the total launch market, that metric is purposefully misleading. ULA launches a small fraction of the global launches, and they have seen commercial demand crater. The 8 government launches [1] they did fly are from a bygone era where ULA was the sole-source contractor[2]. Starting in 2015, SpaceX has been able to bid, and they win most of those contracts as long as they have the capability. Direct Geosynchronous Orbit missions still go to ULA, since the Falcon 9 rocket did not have the long-duration and high-energy upper stage to accomplish these missions. The demonstration mission for Falcon Heavy validated 2nd stage improvements that will allow SpaceX to compete for these missions. ULA and ULA-friendly congressmembers were able to force through a block-buy to keep ULA afloat for another half-decade. ULA recently declined to bid on upcoming government satellite launches despite the fact the US government pays almost $1 billion per year to guarantee the ability to launch payloads domestically, via the Evolved Expendable Launch Vehicle Launch Capability Contract[3] That is coming to an end soon.

New Space Launch does not mean a New Military-Industrial Complex

SpaceX is not your typical military-industrial complex government contractor. They are not interested in getting money from the U.S. government for everything and anything possible. SpaceX has a few narrowly focused goals, and they have used governmental programs to further them.

The company was founded in 2002 to revolutionize space technology, with the ultimate goal of enabling people to live on other planets. - SpaceX Mission Statement

SpaceX has competed and won several development contracts to help fund the initial development of their launch vehicles.

- Commercial Cargo Development: $396 million for development of Cargo Dragon and F9 v1.0. Future versions were developed with internal funds.^

- Commercial Crew integrated Capability: $440 million for Crew Dragon development

- Commercial Resupply Services: End result of Commercial Cargo Development, provides cheaper cargo launch to ISS for NASA

- Commercial Crew Transportation Service: Return astronaut launch capability to US, do it cheaper than Boeing[4], Soyuz, or the Space Shuttle.

Another key point is that all of these contracts required outside investment from the commercial partner. None of them were sole-source and none were cost-plus. They allowed NASA to leverage private investment to offset their own budget. And for the SpaceX naysayers that say SpaceX is subsidized by the government, all of these programs resulted in lower-cost of service to the U.S. government saving billions, as well as bringing in a significant chunk of the global commercial launch market back to U.S. soil, offsetting government spending and providing a sustainable commercial space industry. Every commercial launch from US soil brings revenue to the US that might have gone to China, Russia, or Arianespace.

Old Space is in a corner, rather than cornering Space

From that perspective, SpaceX is crushing the competition in the sectors it enters. Russia have officially given up[5]. ULA is unlikely able to compete with Vulcan. SMART and ACES are 5-10 years away still while New Glenn and (almost fully) reusable[6] F9 are almost here. Arianespace is feeling the heat, and the Director General of the ESA says building Ariane 6 may have been the wrong move. Framing the discussion that shows incumbent government contractors in a healthy position is dishonest, because when they compete against the commercial sector they lose, badly.

The New Space Inversion

SpaceX and Blue Origin are not building spy satellites. They are not trying to build one-off research projects for DARPA. They are building rocket transportation technology at low-cost, and at scale, with technology and efficiency that cannot be beat by the Old Space market. To try to view their achievements outside that lens is rather foolish.

The real threat to these sectors does not come from the established New Space companies, but rather the rising tide of private investment in space startups. Over $3.9 billion was invested in space in 2017, more than any other year, and it is predicted to grow even more going forward. The principles of rapid innovation and low overhead are the real threat to incumbent companies. The real question we should be asking is if Old Space can adapt quickly enough to compete. New Space has proven it can compete against, and dominate, Old Space in some areas.

It is an exciting and positive time in the space industry. Feats thought impossible a few years ago are now commonplace. However, it is important to be honest about the realities of the industry and the true changes taking place. Companies that ignore these signs could find themselves at the back of the New Space Race pack.

1 launch was for a commercial company, Orbital ATK, for their Cygnus capsule, but this was for a government customer, NASA ↩︎

ULA pushed for a 5 year block-buy of rocket cores in 2014. This was conveniently right before F9 was certified for DoD launches. Both parties entered mediation where the US promised to accelerate certification and allow SpaceX to compete for a few launches competitively. ↩︎

The ELC is guaranteed funds paid to ULA every year no matter if ULA launches. However, ULA 'pays back' the ELC whenever they launch a rocket, and ULA argues that means it is not a subsidy ↩︎

For the exact same number of missions and crew delivered to the ISS, Boeing costs $3.27 billion at $418 million per flight, versus SpaceX's $2.2. billion at $308 million per flight ↩︎

Dimitry Rogozin, Deputy Prime Minister of Russia, recently said that commercial space launch is not worth competing against SpaceX and China, finalizing the decline of Russia as one of the top launchers of commercial payloads to a sideline player. ↩︎

SpaceX is close to perfecting recovery of the fairings of Falcon 9, which would lead to another 10%-15% cost reduction in launch. Elon Musk recently unveiled plans for recovering the F9 second stage using an inflatable ballute system. Block 5 of F9 which promises 10 flights with minimal refurbishment is launching May 4th. ↩︎